IR35 Timeline: From Conception to Full Implementation

March 23rd, 2024

IR35 is a crucial piece of legislation that all UK-based businesses need to be aware of. In preparation for its full implementation, we have put together a timeline of IR35 developments for context.

The world of work is changing fast, and with modern concepts such as the ‘gig economy’ taking shape, HMRC has set out to establish regulations that will force companies to make a clear distinction between their employees and independent contractors (or self-employed workers).

HMRC’s answer was to introduce legislative framework known as IR35, aimed at addressing the complexities and potential for tax avoidance within this changing work environment. IR35, formally known as the Intermediaries Legislation, was unveiled in 1999 and first implemented in 2000, but there have been many changes since then and, with changes being implemented recently, IR35 is now coming into scope for all businesses that operate in the UK.

We have put together a comprehensive guide to IR35, sharing everything businesses need to know to stay compliant and gain access to the benefits of engaging a self-employed workforce.

Furthermore, Briars’ CEO Andrew Fahey has recorded a podcast on IR35 with Michael Cleaveley, the founder of CoComply. Sign up here to be the first to know about the launch of this episode.

Our thesis on IR35 is that HMRC is likely to take a positive view of businesses that have tried to do the right thing in IR35 implementation, have gone through a suitable due diligence process and have implemented any required changes. They refer to this as reasonable care within the legislation.

Our guide is relevant for all businesses that either already operate in the UK, those who want to expand their UK operations, or those thinking of entering the UK market for the first time. Meanwhile, similar regulations are being implemented in many global markets, so staying up to date with IR35 is crucial for all international expansion planning.

IR35 Timeline

In this post, we will aim to set out the timeline of IR35 changes as they have occurred over the years, providing you with key context to this legislation.

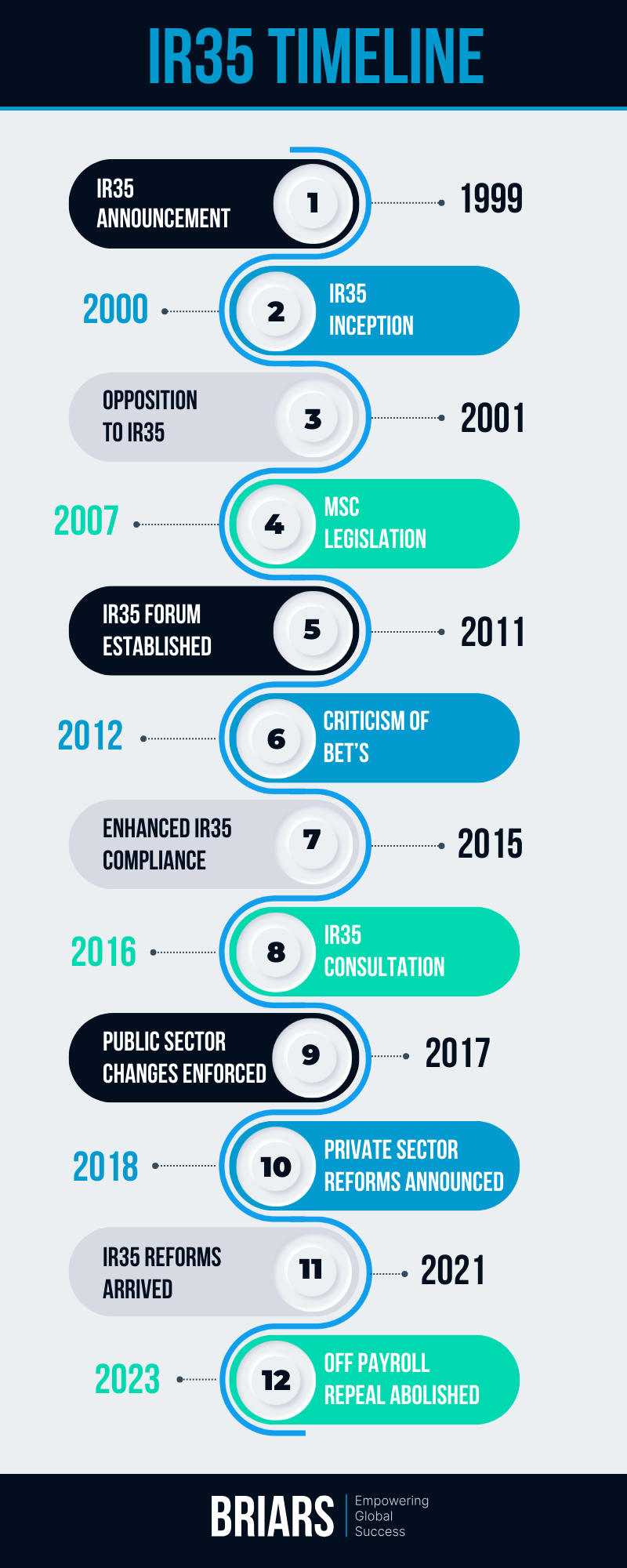

IR35 Announcement in 1999

The journey of IR35 legislation began in 1999 when the UK government announced its intentions to introduce a new set of tax regulations. This announcement aimed to address the issue of ‘disguised employment,’ where individuals would use intermediaries, such as limited companies, to perform services but operate in a manner similar to employees, thereby gaining tax advantages.

The Inception of IR35 Legislation in the Year 2000

In the year 2000, the IR35 legislation officially came into force. This pivotal moment marked the government’s effort to combat tax avoidance by ensuring that workers, who would have been deemed employees if they were providing their services directly, paid similar taxes to actual employees. The legislation targeted those operating through intermediaries within the private and public sectors, prompting a significant shift in how contractors and freelancers managed their taxation.

Objections to IR35 from 2001 to 2010

Between 2001 and 2010, IR35 faced substantial opposition from various stakeholders, including contractors, freelancers, and business owners. Critics argued that the legislation was complex, difficult to comply with, and unfairly penalised genuine small businesses. This period was marked by legal challenges, protests, and calls for reform, highlighting the contentious nature of the legislation and its impact on the contracting community.

The Proposed Overhaul of IR35 in 2011

In 2011, acknowledging the widespread criticism and the complexities surrounding the enforcement of IR35, the government announced plans to overhaul the legislation. This proposal aimed to simplify the rules and improve the way IR35 was administered, with the intention of making it easier for genuine businesses to comply while still targeting disguised employment effectively.

Strengthening Compliance to IR35 in 2015

By 2015, the government introduced further plans to enhance IR35 compliance. This initiative sought to refine the administration of the legislation, focusing on improving guidance, resources, and tools for both contractors and the entities engaging them. The aim was to provide clearer pathways for compliance, thereby reducing the burden on small businesses and independent professionals.

Implementation of IR35 in the Public Sector in 2017

The year 2017 saw the extension of IR35 rules into the public sector. This significant development transferred the responsibility for determining IR35 status from the individual contractor to the public authority, agency, or third party engaging them. This shift marked a new era in the enforcement of IR35, aiming to ensure that workers who effectively operate as employees, albeit through a company, pay employment taxes similarly.

The Advent of IR35 in the Private Sector Between 2020 and 2021

The rollout of IR35 regulations was extended to the private sector between 2020 and 2021, amidst much debate and concern from the business community. This extension mirrored the changes made in the public sector, placing the onus on large and medium-sized companies to determine the employment status of their contractors for tax purposes. This move aimed to level the playing field between employment statuses and ensure tax fairness across the board, despite the challenges and controversies it ignited.

IR35 in 2024 and Beyond

It’s a fact that IR35 has come into force and must be given due consideration. After all, it reshapes contractual engagements, influences financial planning, talent strategies and necessitates a thorough understanding of compliance requirements.

With changes and updates to the legislation, especially the 2017 and 2021 reforms shifting the responsibility of determining IR35 status from contractors to the medium and large businesses that hire them, it has become imperative for all parties involved to grasp the nuances of IR35 fully.

Nonetheless, we believe that the market overreacted initially to IR35 announcements, leading to many industries stopping all engagement with independent contractors, which restricted their ability to access talent.

Now the recent IR35 changes have had time to bed in, forward-thinking businesses are engaging their workforce across employees directly, through and EOR and also accessing talent by engaging directly with independent contractors by implementing robust compliance systems.

At Briars, IR35 is one of the many global workforce challenges we help clients to deal with. We offer a Global Workforce Audit to help you gain full visibility of your global workforce and deal with any regulatory challenges before they emerge. Get in touch now for a consultation.

Shaun Cumming

Shaun is Head of Marketing at Briars, bringing 15 years of content and marketing leadership experience from his time at global financial services firms such as BlackRock, BNY Mellon, Brooks Macdonald and Investec. At Briars, his mission is to tell the story of our company and its people, as well as to shape the brand as we head into a new phase of growth. Shaun is leading the talented marketing team and is a member of our Senior Leadership Team.

Copyright © 2024 Briars Group | All Rights Reserved | Read Our Cookie Policy